A “Condensed” Milk Expansion May Support Profitability in 2024

As the calendar flips to 2024, U.S. dairy producers face numerous mixed signals up and down the dairy supply chain. On the one hand, domestic demand remains robust, buoyed by an insatiable U.S. appetite for cheese, yogurt, and other dairy goods. On the other hand, export demand has softened as economic woes have emerged in a few key dairy import markets. Combined, these competing factors have led to elevated uncertainty in the sector.

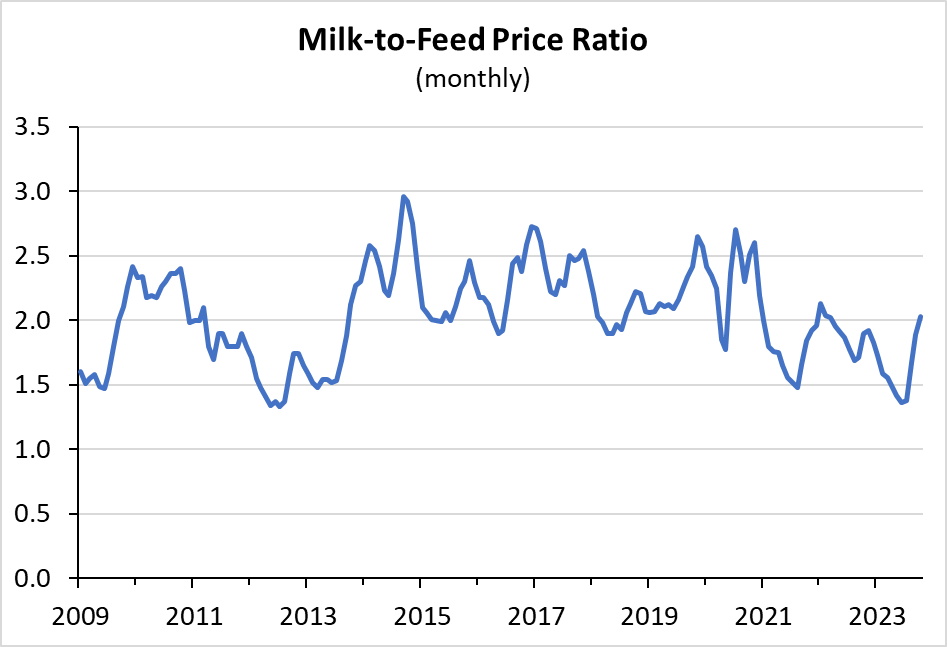

If viewed through a microscope, the trend in 2023 milk prices might indicate financial stress for dairy producers. Indeed, the rapid price drop last year, combined with elevated feed costs, triggered significant Dairy Margin Coverage (DMC) payments to producers. DMC payments topped $1.2 billion through November 2023, peaking in mid-2023. In June 2023, the milk-to-feed price ratio dropped to 1.36, its lowest level since the mid-1980s save for a blip in 2012. Fortunately, the ratio has since reversed, rising above 2.0 in December as feed costs declined and milk prices rose. Still, the ratio remains below its 20-year average of 2.26, underscoring the compression in dairy sector profitability over the last year.

Will Dairy Prices Stabilize in 2024?

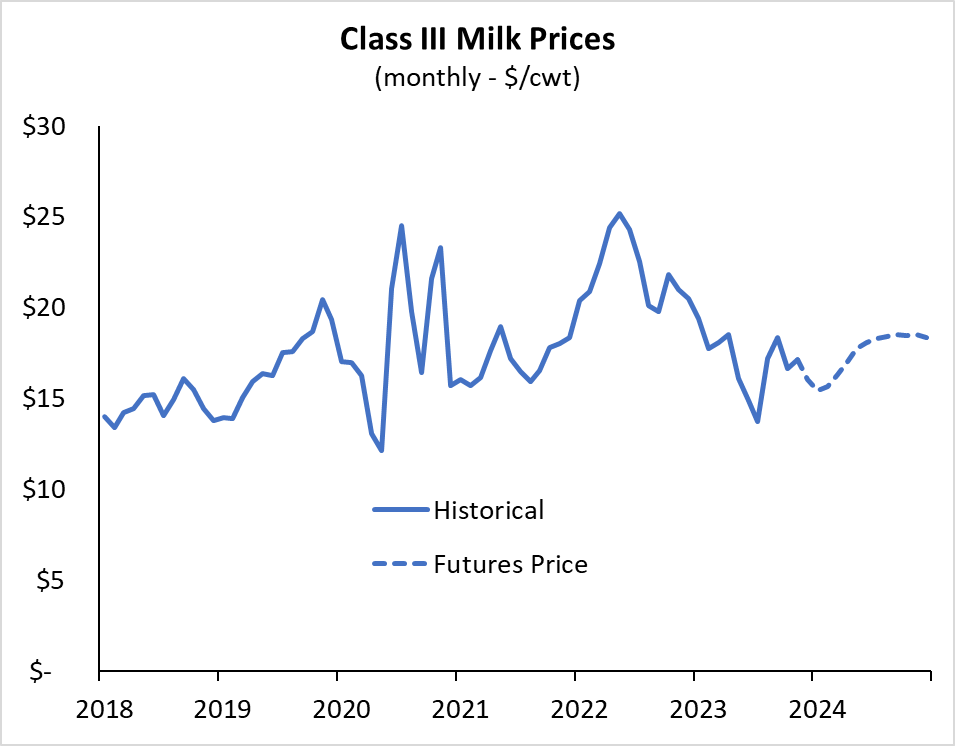

During the last few years, one of the only constants for U.S. dairy prices has been change. Class III milk prices bounced higher and lower in response to the COVID-19 pandemic and subsequent government programs aimed at boosting dairy demand. When those effects wore off, strong export demand, rising feed costs, and a contraction of the U.S. beef cattle herd helped push prices to record levels in 2022. Class III milk prices peaked above $25 per hundredweight in 2022 before dropping rapidly in 2023, declining by as much as 50%. At this time, prices remain volatile but have since recovered from the lows experienced last year, much to the relief of producers.

Looking ahead, market data suggest milk prices could stabilize this year, potentially at marginally higher levels. As of early January, the average Class III futures market price for the year was $17.59, above the $17.09 average for 2023. The USDA’s projection in the January WASDE was less optimistic, but still showed Class III prices averaging $16.10 in 2024. There is certainly reason for optimism, given the limited expansion in the sector over the past two years and the broad decline in feed prices. However, higher labor costs and declining export volumes also portend a headwind.

Pullback in Exports

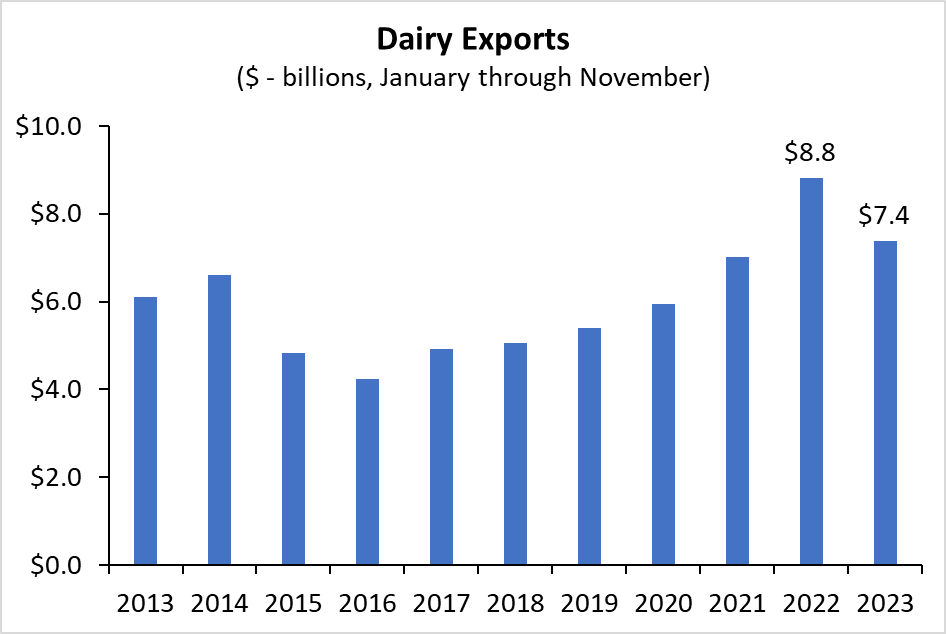

One of the notable contributors to declining dairy prices last year was reduced export demand. Export volumes of U.S. dairy products dropped 6% in 2023, partly due to weaker Chinese import demand for whey and cheese. Through November, dairy exports were $1.4 billion lower in 2023 than at the same time in 2022, including $140 million less to China. Acknowledging last year’s slowdown, the USDA currently projects U.S. dairy export volumes will bounce higher in 2024. Its current forecast shows export volumes rising nearly 7% in 2024. It is important to note that the total value of U.S. dairy exports could still decline this year if the unit value prices are low enough. However, substantial export volumes would help limit a buildup in domestic inventories. Indeed, the USDA currently projects U.S. dairy inventories will decline 5% over the next 12 months. Higher exports and stable domestic inventories could provide support for prices.

Modest Supply Growth Supporting Prices

Fortunately for U.S. producers, tepid export demand has been partially offset by limited expansion in the sector. After increasing a meager 0.1% in 2022, the USDA projects milk production grew by only 0.2% in 2023. The growth rate in both years was well below the average of 1.3% annual growth from 1970 to 2021. Dairy producers have been relatively restrained in increasing production due to elevated feed costs, challenges in sourcing labor, and greater financing costs associated with building new barns. Many of these challenges are unlikely to be resolved in the near term. As a result, the USDA projects a modest 0.9% growth in U.S. milk production in 2024.

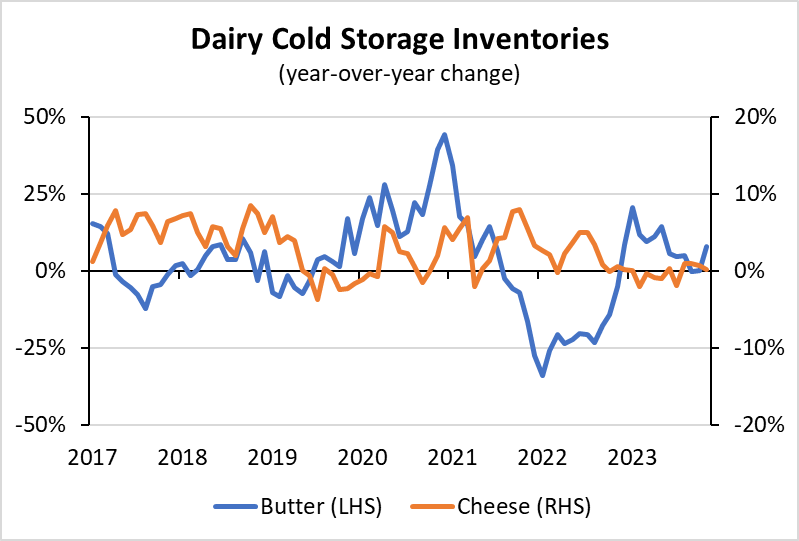

One benefit from slow dairy production growth has been a limited buildup in U.S. dairy inventories. Butter inventories at the end of November were 8% higher than last year, while cheese inventories were unchanged. Cheese inventories are nearly seven times larger than butter inventories, though, so total inventories increased a relatively modest amount. U.S. dairy stocks in cold storage have stayed relatively stable despite the export slowdown.

Conclusion

The challenge in determining where dairy sector profitability may head in 2024 stems from competing headwinds and tailwinds. Feed costs have declined recently due to the recovery in global annual crop inventories. However, feed prices remain elevated and could bounce higher in 2024 if a dry winter causes hay prices to spike. On the demand front, exports were hindered last year by a tepid global economy and a strong U.S. dollar. This year exports are projected to increase, which should support prices. Ultimately, the limited expansion of U.S. dairy production over the last two years could be a silver lining that supports dairy sector profitability in 2024, if only at modest levels.