U.S. Energy Response to Global Disruption

You don’t have to look hard to find evidence that energy markets are in disequilibrium. West Texas Intermediate oil prices touched 14-year highs in June 2022; retail gasoline prices set new nominal records in June 2022; average U.S. natural gas prices reached a 14-year high in May 2022; and coal prices hit a 35-year high in December 2021. This phenomenon isn’t limited to North America—in March 2022, the International Monetary Fund’s global energy price index set a new nominal record, a function of elevated energy prices in nearly all geographies and across all categories. The fact that current energy prices have yet to surpass 2008 inflation- adjusted peaks is of little consolation to the consumers and industries grappling with higher input costs at every turn. Farmers, food producers, and rural energy providers are sensitive to these markets, but unfortunately, they have little influence over the cause and response to the current global energy disconnection.

Cause

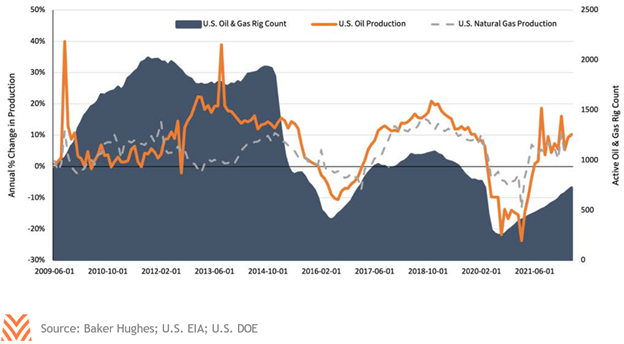

The current energy market situation is a function of several coincident factors. The COVID-19 pandemic all but halted global economic activity in March and April of 2020. This sudden slowdown created a chain reaction that led to a dramatic oversupply of oil; in April of 2020 oil futures prices went negative, since there was effectively no place left to store oil coming out of the ground. As seen in the figure below, oil producers responded by capping wells and shutting off production, causing the number of active oil and gas rigs to plummet. As the economy started to spin back up, demand for oil and gas increased but producers hesitated to redeploy capital into new wells and resource discovery. Earnings for the top three oil production companies in the U.S. set historical records in 2021, but cash flow for capital investment was near 15-year lows and cash flows to investors in the form of stock buybacks and dividends set a new 15-year high. Meanwhile, oil producers returned capital to investors rather than invest in new production.

In the March 2022 Federal Reserve Bank of Dallas energy production survey, 59% of executives of publicly-traded oil companies cited investor pressure as the primary reason producers were not ramping up production faster. In that same survey, respondents cited labor shortages and supply chain snarls as additional headwinds to production. Finally, the global response to the Russian invasion of Ukraine included many sanctions and embargos on Russian oil, which exacerbated the global supply shortage.

The Path Forward

As with most complex problems, there is no easy fix to the current global energy situation. Even if there were a swift resolution to the Russia-Ukraine conflict, international energy trade is already being rerouted, with European nations looking for new sources of oil and gas. Meanwhile, U.S. energy infrastructure is aging rapidly, and new oil and gas discovery projects face an uphill battle given that many investors are rotating out of fossil fuel investment and into renewable energy projects. While renewable energy is certainly a big part of the future, there are logical constraints on how much and how fast that capacity can come online. Solar, wind, and biomass-generated power should continue to decrease in cost relative to fossil fuel- based production, but the supply chain, parts, and labor necessary to complete the massive electric transformation may be stretched thin in the coming years. In the meantime, electric vehicles will likely continue to gain in popularity in the U.S., but may continue to be limited by the availability of battery minerals and charging infrastructure.

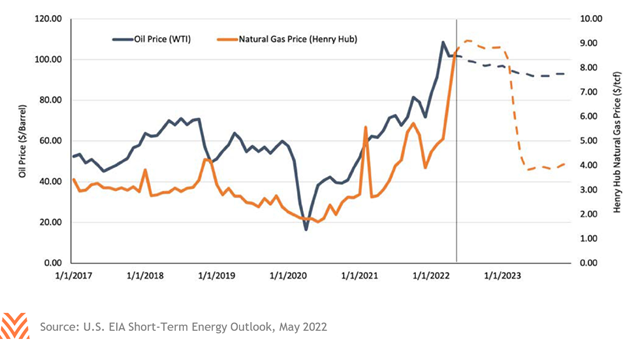

Low supplies with limited substitutes are likely to keep energy prices high for the near and intermediate terms. The U.S. Energy Information Administration forecasts elevated oil and natural gas prices for the remainder of 2022 and into early 2023. Their forecasts call for increases in production to take hold in mid-2023, and natural gas prices may fall faster than oil if supply can rebound more quickly. Electricity producers have few gas-to-coal plant switching opportunities, and Bloomberg New Energy Finance projects that solar and wind generation capacity in the U.S. will increase between 30 and 40 gigawatts in each of the next two years, a sizable increase—but only roughly 5% of total U.S. electricity generation capacity. Until domestic and global supplies stabilize, energy production will likely take an “any-and-all” approach with additional supply from fossil fuels and renewables. Finally, these forecasts indicate continued pressure on fertilizer and fuel costs for producers into 2023, although the rate of increase is likely to moderate later in the year.