The Callable Curve: What’s Been Driving Ag Interest Rates

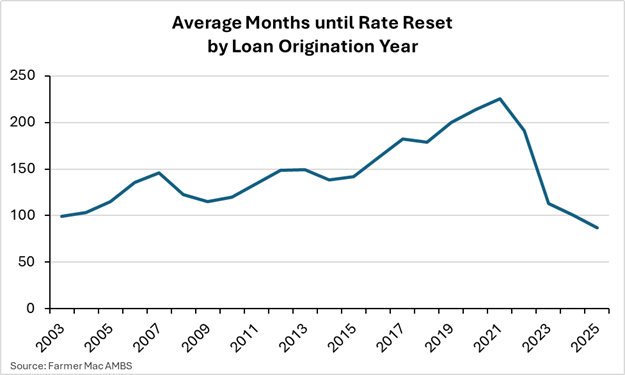

In our Winter 2025/2026 issue of The Feed, the article The Great Loan Shortening highlighted a shift in loan preferences among producers: As interest rates increased across the yield curve from 2021 to 2023, producers began selecting loan products with significantly shorter interest rate resets.

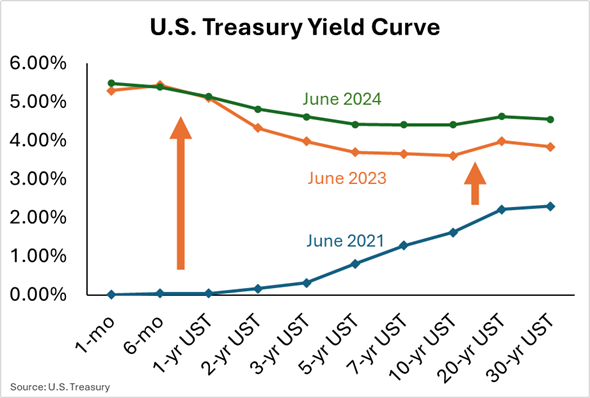

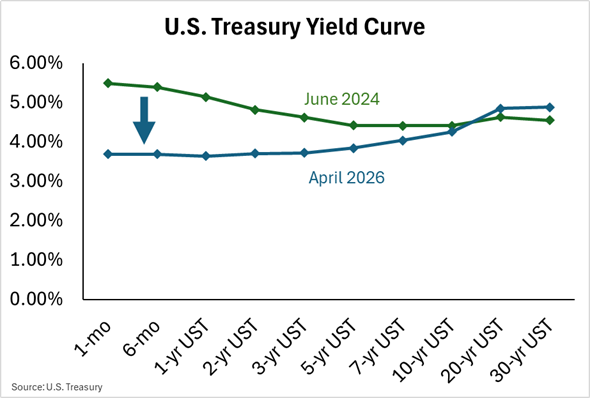

When considering only U.S. Treasury (UST) benchmark rates, this loan-selection phenomenon appears counterintuitive. Producers began selecting shorter-duration loans after the yield curve inverted (when the short end of the yield curve rose higher than the long end of the yield curve). In June 2023, the 1-year UST implied rate was above 5.00% while the 10-year UST implied rate was approximately 3.60%. However, the U.S. yield curve does not fully reflect the interest rates farm borrowers pay.

Issuing Bonds to Fund Farm Mortgages

The driver behind the rise in popularity of shorter-duration loans is multifaceted. First, as the Federal Reserve began raising interest rates in 2022, producers hoped they would shortly decline. Indeed, the Fed Futures market in 2023 indicated that markets expected the Federal Reserve to begin cutting interest rates as inflation was declining. It is plausible that borrowers did not want to miss out on potential interest rate declines by being locked into long-term, fixed-rate loans.

A second, perhaps equally important, caveat regarding the UST yield curve is that it does not directly reflect the interest rates available to farm borrowers. Agricultural lenders derive their funds for loans from numerous sources. For many of the largest agricultural lenders—including the Farm Credit System, Farmer Mac, and others—the bond market provides funds. Each of these organizations works to match bond issuance with loan demand, and fluctuations in bond market yields can flow downstream in the form of higher or lower interest rates for producers.

A Callable Spike

For simplicity, we can examine the impact of bond market fluctuations on a simple 10-year, fixed-rate farm mortgage. We can assume that the interest rate the farmer pays is generally the yield on a 10-year, fixed-rate bond plus a lender spread. In this example the lender issues a 10-year bond to fund the loan. The complicating factor is whether the bond is callable, meaning it can be redeemed early. If the borrower repays the loan over the full 10-year term, a lender can fund the loan with non-callable bonds. However, it is common for farm mortgages to refinance before the end of their term, necessitating the lender to fund at least a portion of the loan with callable debt.

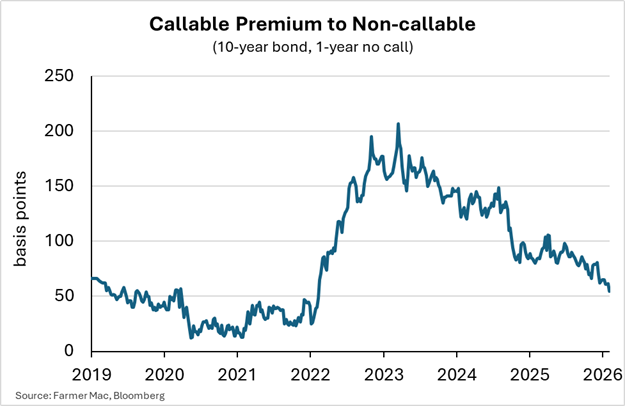

The necessity to fund loans with some callable bonds has led to higher long-term interest rates for borrowers. The graph below highlights the issuance cost premium for callable 10-year bonds relative to non-callable over the past seven years. At peak levels, the interest rate on callable bonds was over 200 basis points higher than that of non-callable bonds. Unfortunately for producers, that increased lender funding costs, which were then reflected in the interest rates they received on their new loans.

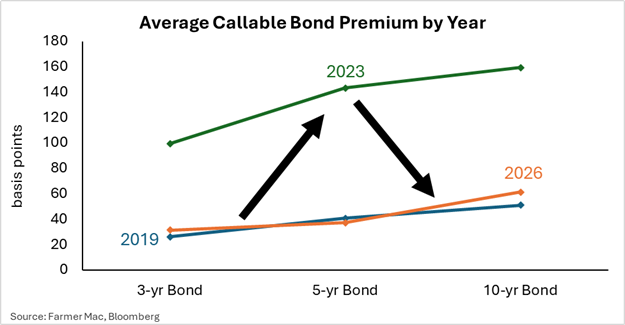

This trivial example of a 10-year, fixed-rate loan illustrates how the bond market compounded the impact of already rising interest rates. In practice, though, lenders rarely fund individual loans with individual bonds. Instead, a mix of bond issuance is used to achieve attractive interest rates for borrowers while also protecting lenders from an asset-liability management standpoint. In recent years, funding mixes have also been calibrated to help mitigate the impact of the callable premium spike, albeit to varying degrees of success. This is due to bonds across the maturity spectrum all experiencing spikes in callable premiums. The “callable curve,” a spin on the UST yield curve, illustrates the spike that peaked in 2023 before trending back close to pre-COVID levels by early 2026.

Callable Premium Normalizing, But Not Demand for Short Duration Loans

As markets predicted, the Federal Reserve did cut short-term interest rates numerous times over the past two years. With the UST yield curve no longer inverted, the premium for callable bonds has also dropped considerably. The premium on a 10-year callable bond fell to approximately 50 basis points in February, roughly one-quarter the level of just a couple of years ago.

Despite a lower callable premium and lower long-term interest rates for producers in general, loan selection continues to favor shorter-duration loans. What’s fueling the behavior today is likely something different. Notably, a compression of farm operating margins has forced producers to focus intently on cutting costs. While fertilizer, seed, and chemicals often constitute a larger expense line item than interest costs, producers are often limited in their ability to alter those costs. With borrowing costs, though, selecting a shorter-duration loan in the current market environment can quickly reduce interest expense on an income statement.

Outlook

The USDA Farm Income forecast released in February showed that crop margins are likely to remain compressed for many producers in 2026. This may lead to continued interest in shorter-duration farm loans as producers look to cut costs.

Are there risks to this trend? If the yield curve rises dramatically in the coming years, producers who select shorter-duration loans today likely face significantly higher costs when their loans are repriced. The outlook for interest rates is unclear, though, especially given the nomination of a new Federal Reserve chair in January 2026. If the yield curve remains steady or drops though, borrowers who select shorter duration loans today might benefit both now and in the future.