Southbound Surge: U.S. Corn Exports Gain Momentum in Mexico

The outlook for annual crop growers in 2026 remains murky as the growing season approaches. While the USDA forecasts that Net Cash Farm Income will increase modestly this year, propelled higher by historic government payments, expenses remain elevated and crop sector revenues stagnant, suggesting many producers may just be treading water. There are positive developments, though, for annual crop producers following the record corn harvest in 2025. Specifically, a surge in export demand has helped provide support for both corn futures prices and Midwest basis levels.

All Aboard the Grain Train

As the size of last fall’s corn crop has come into clarity, focus has shifted to where all those bushels will go. The USDA made its final adjustment to the estimated 2025 crop size, showing U.S. producers harvested 17 billion bushels—14% higher than 2024 and the largest crop on record. As the estimated crop size has increased over the last 6 months, so has the pressure on prices. The December 2025 corn futures contract declined nearly 10% from its peak in February to the contract settlement. The pressure on prices was amplified by the question: Where will demand for all the corn bushels come from?

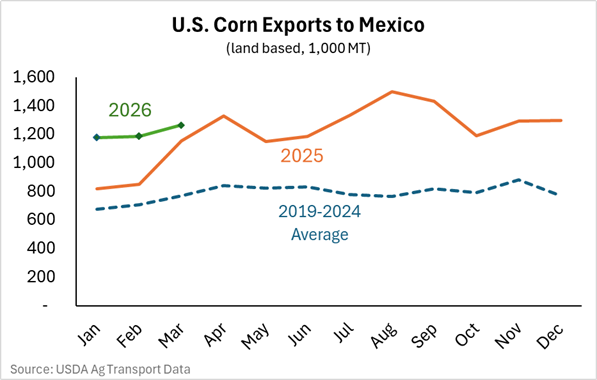

One significant new source this marketing year is actually an old one, just on a grander scale. U.S. corn exports to Mexico have been vigorous this winter, surpassing all previous records thus far. Most of Mexico’s corn imports are via rail, and shipments of U.S. corn via rail rose to 3.6 million metric tons (MMT) in Q1 2026. This was 29% higher than Q1 2025 and 69% higher than the previous 5-year average.

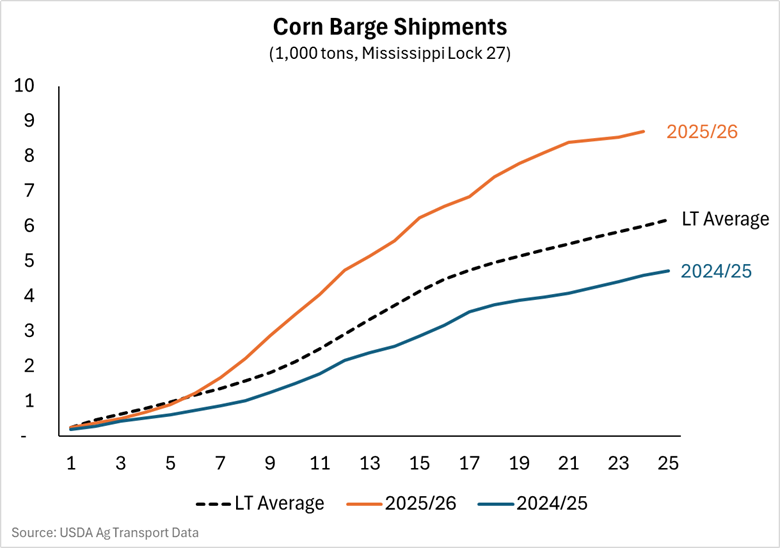

Robust export shipment volumes have not exclusively been via rail into Mexico. Corn barge shipments down the Mississippi were also elevated this winter, with a portion ending up in Mexico. Corn exports via barge have also increased to other countries during this marketing year, including Japan, South Korea, and Taiwan. While grain from the Upper Midwest often flows west via train before being exported to Asia, ample supplies across the Midwest have led to a steady flow of corn exports down the Mississippi this winter as well.

Basis Boost

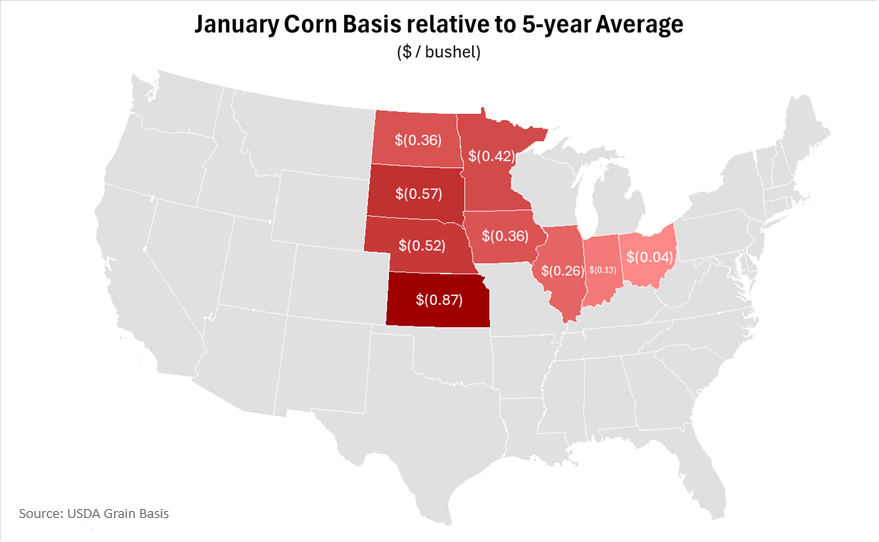

Elevated export volumes have done more than support prices; they are also helping lift basis levels. Basis is the difference between the local cash price a producer receives and the price of the relevant futures contract. Regional variation in basis can reflect transportation costs, but basis also tends to reflect regional supply and demand dynamics. A record U.S. corn crop and the resulting higher inventory amounts have caused basis levels to be significantly lower than normal this marketing year across most major corn production states. The average January corn basis ranged from approximately one nickel lower in the Eastern Corn Belt to over $0.85 lower in Kansas, relative to the 5-year average.

Basis levels have started to recover in response to strong export demand. It is normal for basis to improve throughout a marketing year as grain buyers reward producers for storage, but as those buyers looked to source additional bushels, basis levels across the Midwest jumped significantly more than normal in February. Average basis levels improved by more than $0.20 on average in February 2026 relative to January 2026. This increase was over five times the average increase between the two months, providing a meaningful boost to farm-level corn prices. While basis levels remain lower than average this marketing year, strong export demand is helping offset producer margin pressure.

Looking Ahead: Assessing the Longevity of Strong Export Demand

The durability of strong corn exports remains an open question. There have been several tailwinds propelling corn exports over the past 12 months. The approximate 10% decline in the U.S. dollar index has made U.S. agricultural exports more affordable relative to other countries, helping most U.S. ag exports. Corn has fared even better, which is partially due to prevention measures focused on keeping the parasitic fly New World Screwworm (NWS) out of the U.S. With Mexico experiencing an outbreak, live cattle imports into the U.S. have plummeted since early 2025, leading to a spike in feed grain demand in Mexico . Indeed, lower feedlot inventories on the Western Cornbelt partially explain why basis has been significantly lower across that region this marketing year. The longer the NWS outbreak in Mexico lasts, the longer U.S. corn exports to the country are likely to remain elevated to feed the live cattle retained there.

All told, the USDA projects corn exports will reach record levels for the 2025/2026 crop. While some factors driving this may be market oddities, such as NWS, other tailwinds remain. A weaker USD, trade agreements signed in 2025, and ongoing trade negotiations for additional agreements may bode well for corn exports this year and years to come. For producers, strong demand cannot arrive soon enough, especially when compiling budgets for the 2026 growing season that show margins are likely to remain under pressure. If corn exports remain on record pace, price and basis may rise to opportunistic levels to sell both this year’s and last year’s crops.