Resilience Under Pressure: Farm Bankruptcy Levels and Implications for Ag Lenders

Farm bankruptcies are rising—but the story of American agriculture in 2025 and 2026 is not one of collapse. It is a story of a resilient sector navigating a difficult down cycle with tools, institutions, and a financial foundation that are meaningfully stronger than in prior cycles. Understanding both the pressure and the context is essential for agricultural lenders seeking to serve their farm customers well and manage their portfolios with clear eyes.

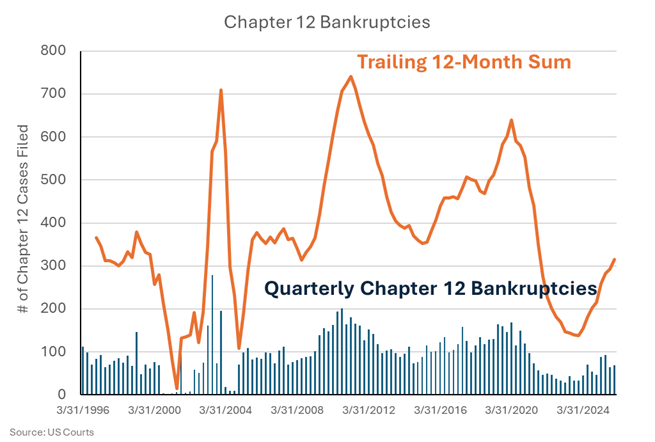

According to U.S. Courts data, there were 315 Chapter 12 bankruptcy filings among family farmers, ranchers, and fishers in calendar year 2025—a 46% jump from the 216 filings in 2024. That headline number deserves context: The current level is nearly half the 599 filings recorded at the prior down cycle’s trough in 2019, and a fraction of the thousands of filings recorded annually during the 1980s farm crisis, which was a fundamentally different event in scale, scope, and severity. The farm sector has faced harder times, and it has come back stronger each time. The question for lenders today is not whether agriculture will endure—it will—but how to support it effectively through a period of genuine, if manageable, stress.

Chapter 12: A Restructuring Tool, Not the Final Word

Before examining trends, it’s worth reframing what a Chapter 12 bankruptcy filing represents. The common assumption that “bankruptcy equals losing the farm” is largely wrong when it comes to Chapter 12.

Congress created Chapter 12 at the height of the farm crisis in 1986, as a debt-restructuring mechanism tailored to the economics of family farming. Unlike Chapter 7 liquidation, which forces asset sales to pay creditors, Chapter 12 allows a farmer to continue operating while proposing a structured repayment plan over three to five years. The process freezes collection actions through an automatic stay, can reduce the principal balance of secured debt to the current market value of the underlying collateral (the ‘cramdown’ provision) along with interest rates to current market levels, and even allows certain tax liabilities, including capital gains from the sale of farm assets, to be discharged as unsecured debt. No other bankruptcy chapter offers this combination of protections for agricultural producers.

The practical effect is significant: A Chapter 12 filer is not surrendering but rather using a federally designed legal tool to convert high-pressure, short-term operating loans into longer-term, land-secured debt structures—buying years of breathing room that informal lender negotiations rarely provide. As one Iowa bankruptcy attorney described it, many Chapter 12 filers are effectively “borrowing money on the land” through the restructuring process, resetting the financial clock while keeping the operation running.

Approximately 40% of Chapter 12 cases conclude with a successful discharge, meaning the farmer completes the repayment plan and exits bankruptcy with the operation intact. That figure understates the true preservation rate, since many cases are resolved through negotiated settlements before or during the process. For agricultural lenders, this means that a filing, while operationally challenging, frequently results in a restructured—and ultimately more sustainable—borrower relationship, rather than a total loss.

The Current Cycle: Rising Filings, But in Historical Perspective

With that context in place, the current filing trend warrants attention—but in a measured way. The 46% year-over-year increase in 2025 follows a 55% increase in 2024, ending a multi-year period of historically low filings. The Chapter 12 filing rate reached its lowest level in nearly two decades in 2022, due to the 2021–2022 commodity price boom, which allowed many farm operators to pay down debt and rebuild reserves. The current rise in bankruptcy filings may be a reversion from an exceptionally favorable period, not the beginning of something unprecedented.

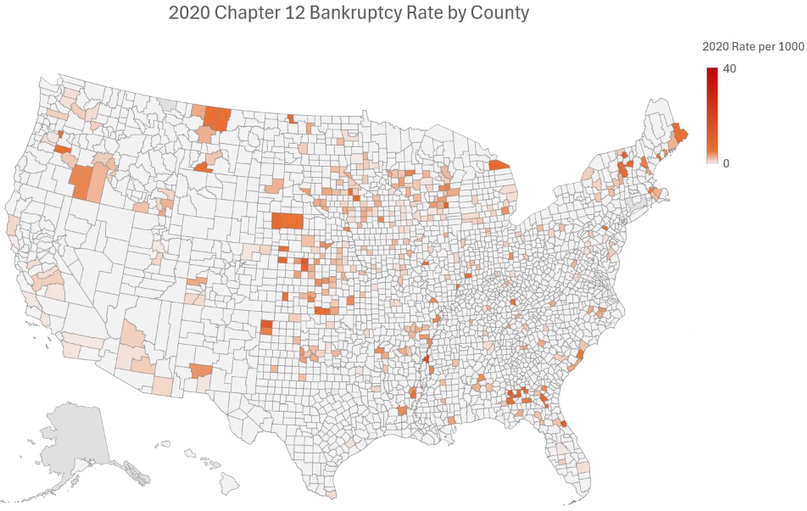

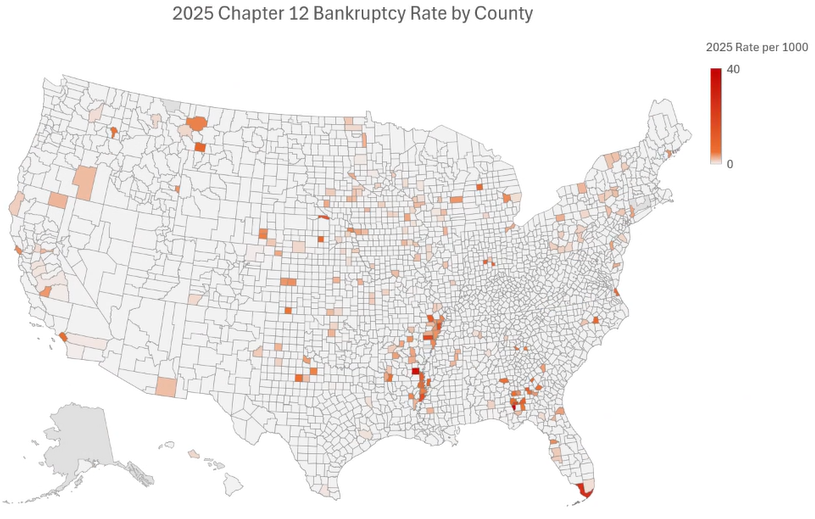

Not only are the absolute levels of Chapter 12 bankruptcies different than the last agricultural down cycle, the geographies of the bankruptcies are also remarkably different. The maps below show county-level Chapter 12 bankruptcy rates for 2020 and 2025. In 2020, farm bankruptcy rates were much higher across the Midwest and generally low for other regions. In 2025, farm bankruptcy rates were highly concentrated in the Delta and Southeast. The concentration of farm revenues in soybeans, cotton, and rice in the Delta is a likely driver of the stress, as U.S. ag exports of those three commodities fell precipitously in 2025. Combined with less cattle production, the Southeast region has a disproportionate exposure to trade-impacted commodities.

Together, the Midwest and Southeast account for more than 70% of 2025 cases. The Midwest recorded 121 filings (up 70% year-over-year) and the Southeast 105 (up 69%). Within those regions, distress is sharpest in specific commodity sectors: rice in Arkansas (33 filings, the state’s highest in the 21st century), row crops and poultry in Georgia (27 filings, up 145%), and corn and soybean operations across Iowa (18 filings, up 220%), Missouri (16 filings), and Wisconsin (16 filings).

Since these spikes are heavily concentrated by sector, lenders with diversified agricultural portfolios and multiple geographies generally have considerably less exposure than these headline figures suggest. Livestock, dairy, and many specialty crop sectors are performing meaningfully better. Net farm income across the broader sector, while declining, remains well above its long-term historical average in inflation-adjusted terms. The current stress is real and concentrated, not a broad-based agricultural collapse.

The proximate causes of rising filings are well-documented. Four consecutive years of declining farm income have eroded the financial cushion built during the 2021–2022 commodity boom. The USDA projects net farm income will decline again in 2026. On the revenue side, corn and soybean cash receipts have fallen sharply. On the cost side, input prices (seed, fertilizer, crop protection, and diesel) have remained elevated well after the inflation peak, creating a persistent margin squeeze for mid-size row crop operations.

Implications for Agricultural Lenders: Challenge and Opportunity

For agricultural lenders, the current environment is genuinely challenging, but offers an opportunity to deepen relationships and position for the recovery that historically follows every farm sector downturn.

On the challenge side, loan quality is softening. Loans rated “less than acceptable” have risen across farm country – including real estate, production, and agribusiness categories. In the Federal Reserve’s Seventh District, loans facing serious repayment risk have reached levels not seen since 2020. Chapter 12 restructurings create extended workout timelines, potential write-downs through cramdown provisions, and increased workload for credit and special assets teams. These are real costs that require real preparation.

On the opportunity side, agricultural lenders who engage proactively with stressed borrowers—before filings and defaults—consistently achieve better outcomes than those who take a reactive posture. Loan modifications, payment deferrals, operating line restructurings, and referrals to extension service resources all represent tools that can help a borrower navigate the current cycle and remain a long-term customer. In prior downturns, the lenders who leaned in during the difficult years built relationships and market share that carried forward for decades.

Collateral fundamentals remain relatively sound. Despite marginal softening, farmland values are historically strong. Lenders with current appraisals and conservative loan-to-value structures have a meaningful cushion. Refreshing appraisals on real estate-secured agricultural loans in affected regions is prudent, but doing so is likely to confirm that collateral coverage remains adequate for the majority of the portfolio.

Conclusion: A Difficult Cycle, Not Yet a Crisis

A 46% year-over-year increase in Chapter 12 farm bankruptcies is a real signal that deserves real attention. The farms and ranches filing today are facing genuine financial hardship, and the conditions driving them—compressed margins, elevated debt, declining income—will not resolve overnight. Agricultural lenders need to take the trends seriously and manage their portfolios accordingly.

But the broader story of American agriculture in 2026 is not one of structural failure. It is one of a sector absorbing a difficult cycle from a position of stronger balance sheets, land values, and legal and financial tools, than in any prior comparable period. Yes, Chapter 12 filings are elevated, but still significantly less than the peak of the prior crisis. When filings reached several thousand annually, they represented a genuine generational emergency. That is not the current moment.

For agricultural lenders who engage thoughtfully by staying close to borrowers, understanding the restructuring tools available, managing concentration risk, and supporting farm customers through the cycle, the current environment offers the chance to build the kind of enduring relationships that define the best agricultural banking franchises in the country. The farms that survive this cycle—and most will—will remember their lenders for a long time.