Farm Income Holds Up in 2026, Thanks to Record Government Support

U.S. farm sector profitability is expected to dip slightly in 2026 compared to last year, according to the USDA’s latest farm income forecast. Net farm income (NFI) is projected at $153.4 billion, down less than 1% from 2025 (around a 2.6% decrease after inflation). While farm profits remain above long-term average levels in real terms, 2026 NFI stands roughly 24% below the record high set in 2022, highlighting how far the sector has fallen since that boom year.

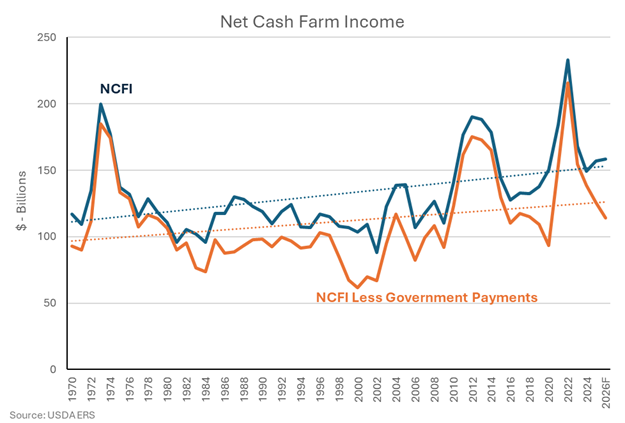

In contrast, net cash farm income (NCFI)—our preferred cash-flow-based metric of the ag economy—is forecast to rise about 3% in 2026 to $158.5 billion. That equals roughly $4.6 billion more than in 2025 (a 1.1% increase above inflation), keeping net cash income above its 20-year average in real terms. This modest growth in cash income, even as overall crop-producer profit edges down, shows that government aid and protein sector profitability are helping sustain farm cash flow amid softer commodity prices.

Government Payments Provide a Critical Boost

Direct Federal payments to farmers are set to soar in 2026, playing an outsized role in income. The USDA forecasts these government payments at $44.3 billion, up from about $30.5 billion in 2025—nearly a 45% jump and the highest farm support in years. This surge stems from expanded commodity price support programs and the rollover of some disaster relief funds from 2025 into 2026. Such infusions are the main reason NCFI is rising in 2026, as farmers’ combined cash receipts from crops and livestock are expected to decline.

The graph below charts net cash farm income over time with and without government payments. Without federal aid, recent farm cash incomes would be significantly lower, underscoring how essential government support has become for the farm economy. Including government support, farm incomes in 2026 are forecast to be above trend; excluding those payments, farm incomes in 2026 are forecast to be below trend.

The USDA’s February update also revises the 2025 figures downward, indicating that last year’s farm income was far weaker than initially projected. The agency now estimates 2025 NFI at $154.6 billion, roughly $25 billion below the September 2025 forecast, and 2025 NCFI at $153.9 billion, about $27 billion lower than previously expected. These steep adjustments reflect how commodity prices slumped and costs ran higher in late 2025, eroding farm earnings.

The revised data shows 2025 production expenses reached $473.1 billion (nearly $6 billion above the prior estimate), while actual government aid was $10 billion less than anticipated due to delayed payments. As a result, the new 2026 outlook starts from a weaker base. Rather than growing from a strong rebound year, farm income in 2026 is forecast to be only flat to slightly higher than 2025’s depressed level.

The protein sector remains a bright spot for the agricultural economy. Robust demand for animal proteins and other animal products is boosting prices for beef cattle and hogs, and the poultry industry is seeing some healing from recent bouts of avian influenza that have dogged many operations between 2023 and 2025. The cost of feed has also moderated significantly, increasing margins for protein producers.

Stubbornly High Farm Costs

Crop farmers are likely to get little relief from input costs. Total production expenses in 2026 are projected at $477.7 billion, essentially unchanged (+1%) from 2025’s record high. Even after accounting for inflation, expenses remain near all-time highs, squeezing profit margins. Labor and interest payments continue to climb, and now fuel and fertilizer costs are again rising. In short, the cost of farming in 2026 is likely to stay historically elevated, so any dip in commodity prices could further pressure profits.

Agricultural debt is also still climbing. Total farm debt is projected to reach $624.7 billion in 2026 (about a 5% increase from 2025), pushing the sector’s debt-to-asset ratio up to 13.75%—the highest in over a decade. Meanwhile, working capital is expected to drop by around 9%. This means farmers are carrying heavier debt loads even as their short-term financial cushion shrinks.

However, farmland values remain resilient, which helps shore up the balance sheet. Land prices continue to trend upward (rising about 4% last year), lifting the overall value of farm assets. As a result, farm equity (net worth) is still growing, projected to increase roughly 3% in 2026. High land equity provides solid collateral for farm loans, offering some protection to both farmers and lenders even as leverage rises.

Credit Conditions and Lender Perspectives

For agricultural lenders, the picture is mixed. Farm credit demand has spiked as margins narrowed. In late 2025,. Many producers are borrowing more just to cover input costs and manage cash flow. Additionally, higher livestock prices are driving greater demand for operating debt.

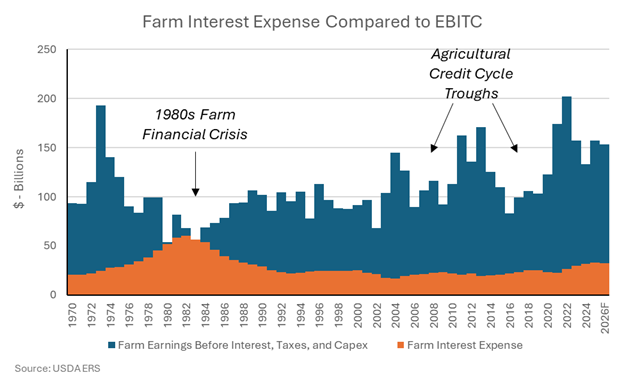

At the same time, interest costs have surged. Annual farm interest expense is expected to top $33 billion in 2026, a record high. Servicing this debt is consuming a greater share of farm income and drawing down liquidity. The chart below illustrates how interest payments now represent a larger percentage of farm operating earnings (EBITC) compared to recent years, signaling that more of farmers’ cash is being swallowed by debt service. Roughly 21% of farm EBITC is expected to be absorbed by interest expenses, up from 12% experienced in 2021.

Signs of financial stress are starting to emerge. Farm bankruptcies jumped by 46% in 2025 (to 315 filings), and loan delinquencies have also ticked up. While high land values keep most loans well secured, lenders are tightening oversight and closely watching repayment capacity and cash reserves. The bottom line: The 2026 farm outlook appears stable but fragile. are propping up the farm sector, but stubborn costs, thin margins, and rising interest burdens mean both farmers and their lenders should pay close attention to economic conditions going forward.