Domestic Drought and Global Production Tighten the Screws on U.S. Farm Margins

As the 2026 growing season begins, U.S. agriculture is facing a convergence of weather-related stress and global market pressure. Widespread drought, depleted soil moisture, and a historically low snowpack threaten crop yields across key U.S. regions, while Brazil is harvesting a strong soybean and corn crop, adding downward pressure on commodity prices. For agricultural lenders, the combination of production risk and price headwinds raises concerns about borrower margins, working capital, and loan performance in the year ahead.

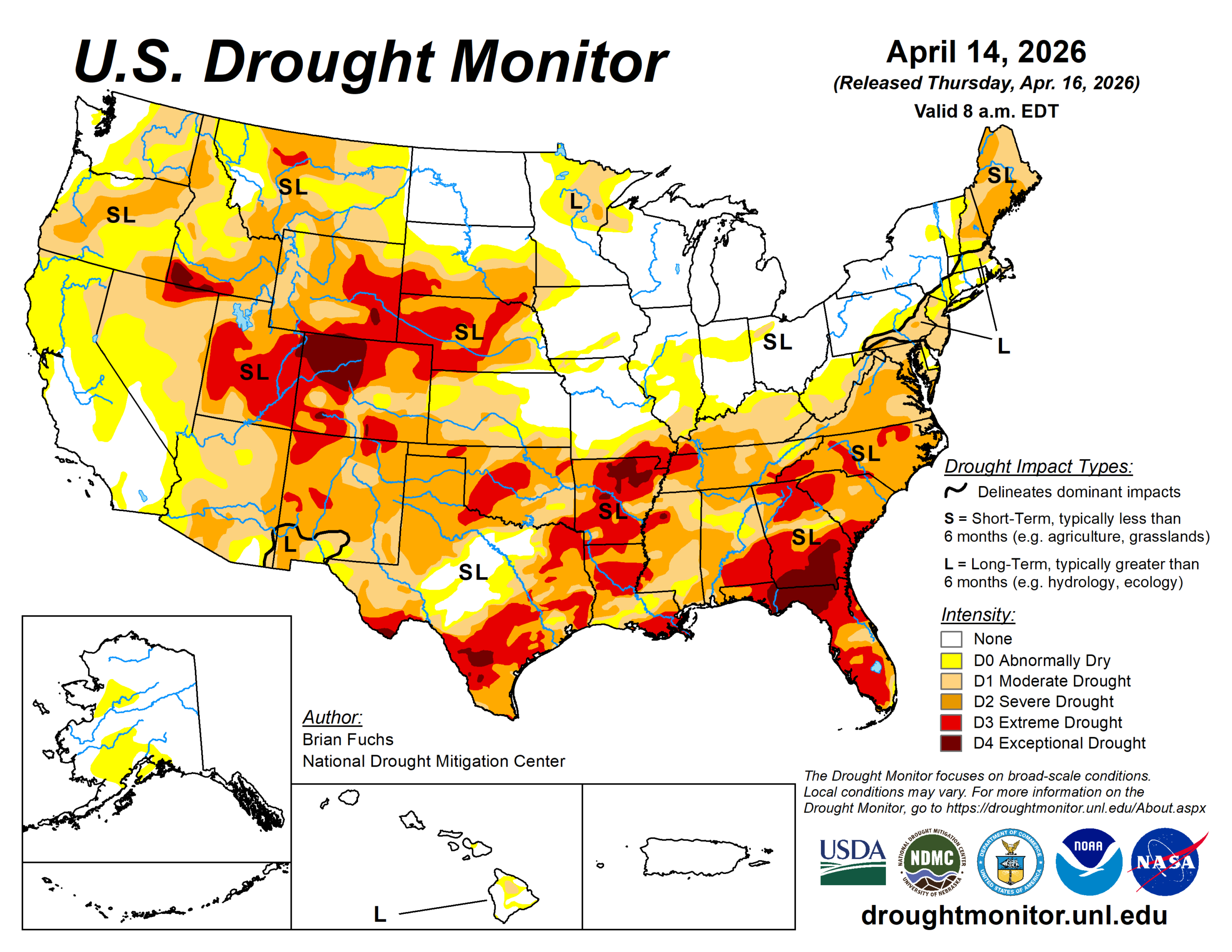

Drought Conditions Deepen Across the U.S.

The latest U.S. Drought Monitor shows over 61% of the Lower 48 states in drought—the widest coverage since late 2024. The Southeast and Southern Plains are particularly dry, with extreme drought conditions in Florida, Georgia, and the Carolinas. Despite some late-February rainfall, long-term deficits persist, and soil moisture remains critically low heading into spring.

In the Southern Great Plains, including Texas and Oklahoma, rainfall since December has been less than half of normal, and unseasonably warm and windy conditions have exacerbated moisture loss. Winter wheat is already showing signs of stress and rangeland conditions are deteriorating. Ranchers are increasing supplemental feeding, and stock water supplies are under pressure.

The Midwest is also unusually dry. Central Illinois and Kentucky recorded one of their driest meteorological winters on record. Farmers report depleted topsoil and subsoil moisture, raising concerns about spring planting and early crop development. Without significant rainfall in March and April, corn and soybean yields could be at risk.

These conditions are already impacting input decisions. Some producers are delaying fertilizer applications or scaling back on seed purchases, which could affect yields and revenue potential. For lenders, this raises the importance of monitoring borrower liquidity and adjusting expectations for 2026 production income.

Western Water Shortages Loom

While California technically entered drought-free status this winter, the state—and much of the West—is facing a “snow drought.” Mountain snowpack, which supplies critical irrigation water, is well below normal. The Sierra Nevada’s snow water equivalent is just 59% of average, and key basins in the Rockies and High Plains are 30–50% below normal. Reservoirs on the North Platte River, which supports agriculture in Nebraska and Wyoming, are only 32–53% full.

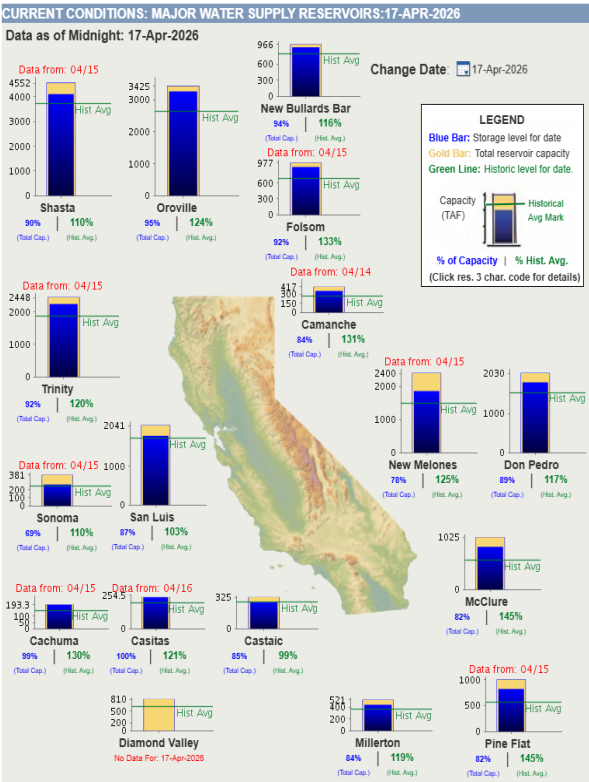

Fortunately for California growers, reservoir levels in the state are currently well above the historical average. The Shasta and Oroville reservoirs were 110% and 124% of historical averages as of mid-April, respectively. California reservoirs will likely have little problem filling near capacity in 2026, even with a lackluster snowpack. However, without a late-season surge in snowfall, irrigation allocations could be sharply reduced in other Western states. This poses a significant risk to irrigated row crops, specialty crops, and livestock operations. Lenders with exposure to irrigated agriculture in the West should prepare for potential yield shortfalls and increased operating costs tied to water scarcity.

Spring Outlook: Some Relief, But Not for All

The National Weather Service’s spring outlook offers some hope for parts of the Mississippi and Ohio Valleys, where above-normal precipitation is forecast. However, drought is expected to persist or worsen in the Southeast, Southern Plains, and Mid-Atlantic. With La Niña conditions lingering, the Southeast may remain dry through the critical early growing season.

For agricultural lenders, this means heightened monitoring of borrowers in high-risk regions. Early signs of crop stress or planting delays could signal the need for revised cash flow projections or operating line adjustments.

Brazil’s Big Harvest Adds Market Pressure

While U.S. producers face mounting weather risks, Brazil’s 2026 harvest is progressing under mostly favorable conditions. The country is on track for a record soybean crop, with widespread rainfall supporting strong yields across central and northern regions. Although drought in southern states like Rio Grande do Sul has reduced output in early-planted fields, later-planted soybeans have recovered. Corn production is also advancing well, with the first crop nearly 60% harvested and the second crop already 45% planted.

For U.S. producers, Brazil’s strong harvest is a bearish signal. The influx of South American supply is likely to weigh on global prices, particularly for soybeans. With U.S. producers already grappling with drought and high input costs, Brazil’s exportable surplus could further erode market share and price competitiveness. This dynamic could compress margins and challenge repayment capacity, especially for borrowers with high leverage or limited working capital.

Financial Implications for Agricultural Lenders

The 2026 season is shaping up to be a test of resilience for U.S. producers—and their lenders. Key financial considerations include:

- Lower yields in drought-affected regions could reduce gross farm income, particularly for dryland operations in the South and Midwest.

- Elevated input costs – especially for irrigation, feed, and fuel – may strain operating budgets.

- Depressed commodity prices due to global oversupply—especially from Brazil—could limit revenue upside even in areas with favorable growing conditions.

- Borrowers with limited liquidity or high fixed costs may face tighter margins, increasing the risk of covenant breaches or repayment delays.

Lenders should consider proactive outreach to at-risk borrowers, stress-testing portfolios under lower price and yield scenarios, and reviewing collateral positions in drought-prone regions. While crop insurance will likely provide some buffer, coverage levels may not fully offset weather-related declines in revenue.