Cropland Acreage

The June Acreage Report is always one of the most market-moving reports that the USDA releases every year, and 2021 was no different. September futures for new crop corn and soybeans both rose over a dollar per bushel after the report was released, though markets pared back those gains in the following days. The 2021 June report showed that the USDA had not moved far off their March prospective planting numbers. Estimated corn acres rose from 91.1 to 92.7 million acres, wheat from 46.4 to 46.7, and soybeans stayed flat at 87.6. This also meant that production estimates for the 2021/22 crop marketing year were mostly unchanged.

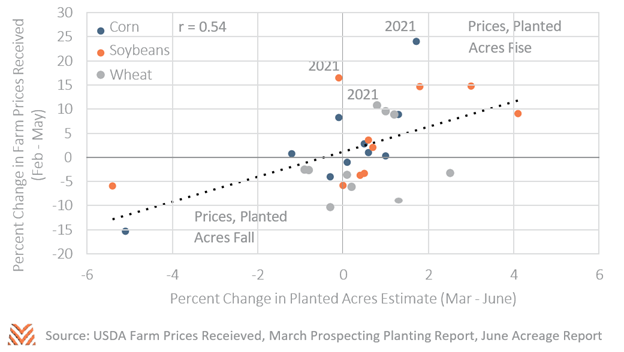

These updated figures were all well below what the private sector expected, and caused the price surge. The cash grain price surge in April of this year meant that all three commodities had seen record percentage increases in farm prices between the two reports. The figure below shows the percentage change in both prices and acreage estimates going back to when the first June report was released in 2012. Historically, price movements have been correlated with changes in acreage estimates between the two reports. A simple linear model of these data suggests that the price changes in 2021 are associated with a roughly 3% increase in corn acres, 2% for soybeans, and 1.3% for wheat. These estimates are all well above the change observed between this year’s March and June acreage reports.

Overall, the new report estimates that total corn and soybean acreage will be 180.3 million acres, just shy of the record 180.4 million acres planted in 2017. Several factors help explain why this acreage estimate may have differed from some industry expectations. One report from the University of Illinois found that USDA data on planting progress and prevent plant acres have been highly correlated with June acreage estimates. In May, these pieces of evidence suggested 92 million acres of corn and 88.6 million acres of soybeans, close to the final June estimate. Despite some indication of higher prices, producers may have been holding back from expanding their operations as much as possible in 2021.

Yet even these other potential means of estimating acreage are not perfectly predictive of the final report’s numbers. Producers have shown a complex decision- making process that adapts to changes in the trade situation, weather, foreign production, policy changes, and a host of other factors that influence global supply and demand. This means that even good models of acreage will have years where they miss the mark. For that reason, the June Acreage Report will continue to be a major market mover and a must-read for agricultural commodity watchers.