American Bankers Association

By Tyler Mondres

Lenders still expect borrower profitability to remain relatively elevated this year.

In 2023, the agricultural economy experienced both a decline in commodity prices as global inventories rebounded and lower export levels relative to 2022. For the broader economy, interest rates increased another 100 basis points as the Fed continued to fight persistent, though slowing, inflationary pressures.

Lender sentiment for the year, as measured by the joint ABA-Farmer Mac 2023 Agricultural Lenders Survey report, largely reflected the corresponding pullback in farm profitability and rise in borrowing costs because of these trends. For producers, lenders expressed concern about liquidity, farm income levels and inflationary pressures. For ag lenders, interest rate volatility remained the top concern, followed by lender competition, credit quality and increased regulatory burden.

Liquidity regained its position as the primary concern among agricultural lenders for their borrowers in 2023, followed closely by farm income levels. These two were also listed as top concerns in 2021 and 2022, highlighting their importance even during periods of elevated profitability. Rising input costs, which were previously ranked as the chief concern in 2021 and 2022, dropped to the third highest this year, reflecting the fact that many input prices peaked in 2022 and have since retreated significantly. The decline in fertilizer prices has been the most notable example, declining more than 50 percent from peak to trough.

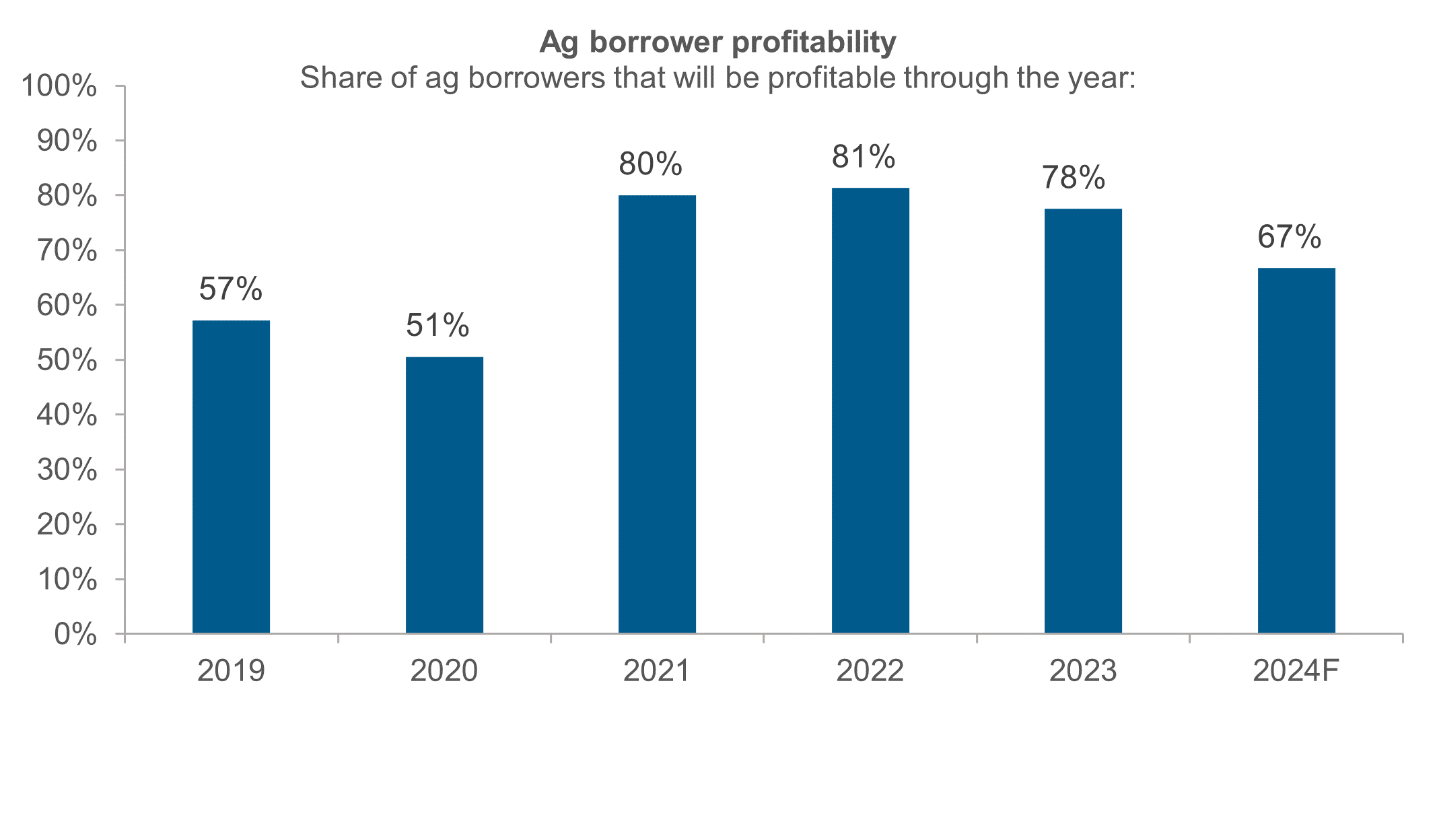

Overall, lenders’ reported concerns translated into a dip in their expectations for producer profitability compared to last year’s record highs. But lenders still expect borrower profitability to remain relatively elevated this year. In 2023, lenders estimate that 77.5 percent of agricultural borrowers will be profitable. While this is a slight decline from 81.3 percent in 2022, it is well above the 51.0 percent and 57.2 percent reported by lenders in 2020 and in 2019, respectively. Lenders do foresee tighter profitability in 2024, as expectations are for 66.7 percent of borrowers to remain profitable next year.

Source: ABA-Farmer Mac Agricultural Lenders Survey, August 2023. Mean response to Q19/20: What percentage of your ag borrowers will be profitable through 2023/remain profitable through 2024?

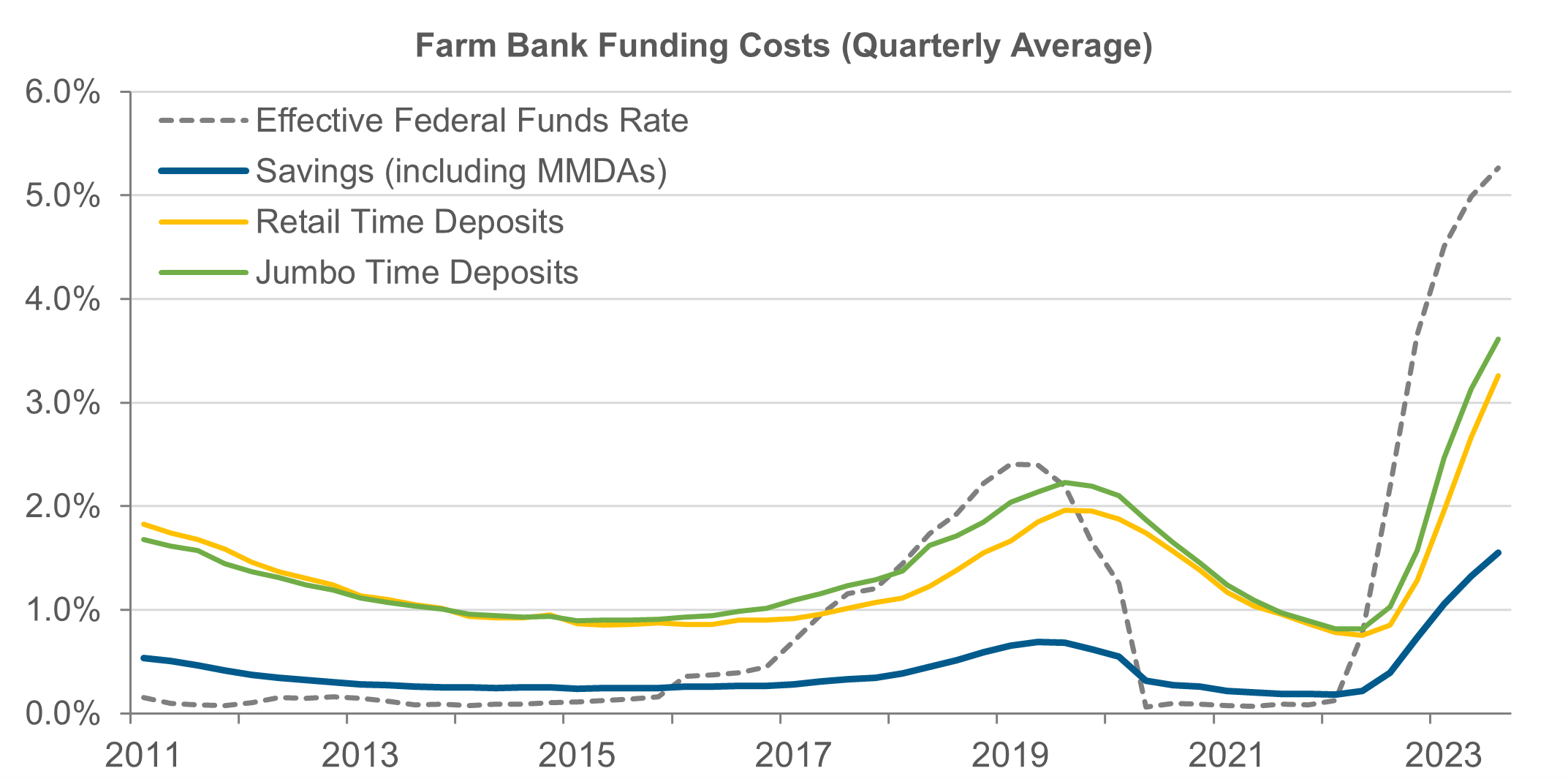

After the Fed hiked rates 525 basis points in just two years, it is no surprise that interest rate volatility remained the greatest overall concern facing lenders’ institutions. More than half of respondents (52.9 percent) ranked interest rate volatility among their top two concerns, up 3.9 percentage points from 2022. While elevated rates and healthy loan demand from farmers and ranchers might support interest income, lenders are feeling the squeeze on interest expense. The average cost of deposits for ag banks, for example, reached a decade-long high in the third quarter of 2023, according to ABA analysis of S&P Global data.

Source: S&P Global, Federal Reserve, ABA analysis. ABA defines agricultural banks as any bank whose farm loan concentration was greater than or equal to the unweighted industry average.

While lender competition remained the second-greatest overall concern in 2023, only one in four respondents ranked it among their top two concerns, down 8.7 percentage points from the prior year. Nearly three-quarters of respondents (72.5 percent) ranked the Farm Credit System as their No. 1 competitor for agricultural loans. Community banks were among the top two competitors for 71.5 percent of respondents, followed distantly by vendor financing (24.0 percent) and regional banks (7.5 percent).

Credit quality concern, which ranked first from 2017 to 2020, was ranked the third-highest concern in 2023 (up from fourth highest in 2022). While agricultural credit quality remains strong, respondents expect some deterioration back to historic levels in the coming 12 months. This is not surprising given the pullback in farm profitability, a trend that respondents expect to continue into 2024. Ag lenders are taking prudent steps to manage these risks. Nearly half of respondents (47.7 percent) reported tightening underwriting standards in 2023, and 42.1 percent reported tightening loan terms.

Increased regulatory burden, which has been a middling concern in prior survey years, became the fourth-greatest overall concern facing lenders in 2023. Heightened concern regarding regulatory burden is likely attributable to the CFPB’s 1071 final rule implementation, which represents a major change to how banks and other lenders process and handle small-business loans—including small loans to farmers and ranchers.

Tyler Mondres is senior director of economic research at ABA.

To view the full article, click here.